The primary investment is negative, so we need to add this to the cash inflow. The management of Health Supplement Inc. wants to reduce its labor cost by installing a new machine in its production process. For this purpose, two types of machines are available in the market – Machine X and Machine Y. summary of federal tax law changes for 2010 Machine X would cost $18,000 where as Machine Y would cost $15,000. The COUNTIF function counts the number of years where the net cash flow is negative. So it would take two years before opening the new store locations has reached its break-even point and the initial investment has been recovered.

How to Calculate the Payback Period in Excel

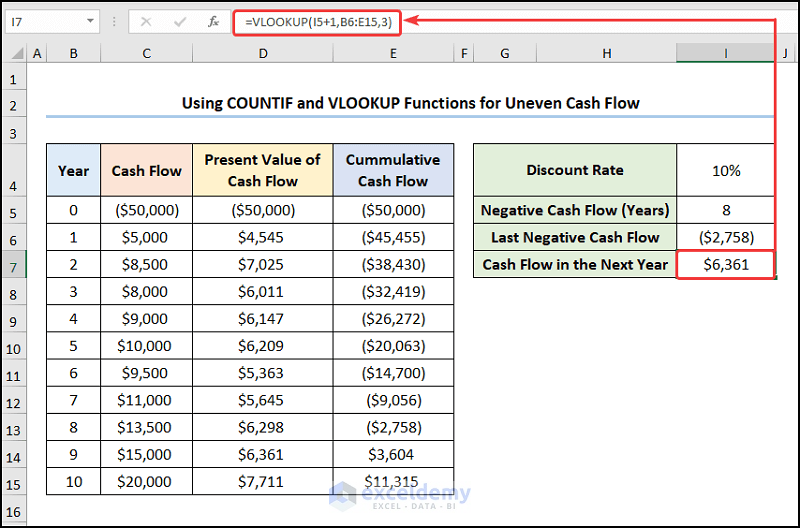

The study of cash flow provides a general indication of solvency; generally, having adequate cash reserves is a positive sign of financial health for an individual or organization. Uneven cash flows are different from uniform or even cash flows, which involve equal payment amounts made or received at regular intervals. With uneven cash flows, payment amounts vary and can be more challenging to analyze and project than even cash flows. Nevertheless, these types of cash flows are common in real-world scenarios like large-scale construction projects, which generate fluctuating revenues over time.

Step 7 – Inserting Chart to Show Payback Period in Excel

As a result, payback period is best used in conjunction with other metrics. Without considering the time value of money, it is difficult or impossible to determine which project is worth considering. Also, the payback period does not assess the riskiness of the project. Projecting a break-even time in years means little if the after-tax cash flow estimates don’t materialize. The table is structured the same as the previous example, however, the cash flows are discounted to account for the time value of money. Conceptually, the payback period is the amount of time between the date of the initial investment (i.e., project cost) and the date when the break-even point has been reached.

- Conversely, the long-time payback period provides a higher cash inflow at a later stage, so more time is required to recover initial investment in comparison.

- Assume Company A invests $1 million in a project that is expected to save the company $250,000 each year.

- This indicator is used not only forthe assessment of project options and business cases in project management butalso for the assessment of investment alternatives.

- If opening the new stores amounts to an initial investment of $400,000 and the expected cash flows from the stores would be $200,000 each year, then the period would be 2 years.

- By calculating how fast a business can get its money back on a project or investment, it can compare that number to other projects to see which one involves less risk.

Payback Period Formula

Next, the second column (Cumulative Cash Flows) tracks the net gain/(loss) to date by adding the current year’s cash flow amount to the net cash flow balance from the prior year. The first column (Cash Flows) tracks the cash flows of each year – for instance, Year 0 reflects the $10mm outlay whereas the others account for the $4mm inflow of cash flows. As a general rule of thumb, the shorter the payback period, the more attractive the investment, and the better off the company would be. The definition of a good or preferable payback period varies, but the general assumption is that the shorter the period the better, because of the liquidity it provides.

Calculating the Payback Period With Excel

The TVM is a concept that assigns a value to this opportunity cost. The Payback Period measures the amount of time required to recoup the cost of an initial investment via the cash flows generated by the investment. In this article, we discuss how to calculate the payback period on an investment with uneven cash flows in Excel.

Posts from: Excel Cash Flow Formula

The payback period is a fundamental capital budgeting tool in corporate finance, and perhaps the simplest method for evaluating the feasibility of undertaking a potential investment or project. Management will set an acceptable payback period for individual investments based on whether the management is risk averse or risk taking. This target may be different for different projects because higher risk corresponds with higher return thus longer payback period being acceptable for profitable projects.

This article will demonstrate two methods how to calculate the payback period in the case of uneven cash flows. The Payback Period method is popular forthe assessment of project options and investment alternatives. It is a ratherlightweight indicator which – thanks to its simplicity – is easy to understandand communicate.

The amount of the initial investment needs to be filled in as a negative cash flow (i.e. an outflow). Even if the initial investment is not an actual outflow, e.g. if it consists of internal cost or resources, it has to be treated as a cash flow for calculation purposes. As the equation above shows, the payback period calculation is a simple one. It does not account for the time value of money, the effects of inflation, or the complexity of investments that may have unequal cash flow over time. Most capital budgeting formulas, such as net present value (NPV), internal rate of return (IRR), and discounted cash flow, consider the TVM. So if you pay an investor tomorrow, it must include an opportunity cost.

Select whether you are projecting even oruneven cash flows, fill in the initial investment and the forecasted net cashflows. The calculator will determine the period in which the initial investmentwill be fully repaid and provide you with the accurate Payback Period (PbP) value. Company C is planning to undertake a project requiring initial investment of $105 million.